Strategic perspective

The creation of strategies and acting strategically places a focus on the long term, and the things that are essential for evolution. Anderson (1999) applies complex systems models to strategic management and concludes that this leads to an “emphasis on building systems that can rapidly evolve effective adaptive solutions.” Strategic direction requires attention to environments and reconfiguration of organizational architecture to fit anticipated adaptation of agents.

The allocation of resources in line with strategic plans ensures that short-term interruptions do not deflect from long-term goals. However, strategies need to be adaptable to changing circumstances. Exploration is fundamental to adaptation and complexity science provides a theoretical basis for empirical findings, in particular, archetypal patterns of strategy, structure and environment (Maguire, 1999).

Strategy and strategic change itself are influenced by the extent to which leaders believe that it is driven by content (that is structure) and by process. Strategies driven by content are influenced largely by the field of economics and focus is on management activities that aim to achieve pre-determined, optimum, rational objectives. These include:

The Strategy-Structure-Performance school, concerned with scale, scope and form of organizations;

The Structure-Content-Performance school concerned with position and market power, and;

Resource-Based View and core competencies.

They are similar in that they make assumption about economic rationality and Newtonian concepts of equilibrium and stability (MacIntosh & MacLean, 1999).

There is now increasing recognition of the importance of key intangible organizational attributes, such as tacit knowledge, learning and intelligence that may signal a more evolutionary view of economics and a demand for a new paradigm focused more on process-driven strategies, essentially challenging the fact that economic rationality should be the primary determinant of strategic behavior. The process-driven school focuses on the extent to which strategy and change are dominated by events and activities that emerge from a wide variety of influences. The school includes: 1. the way that decisions are made, and 2. implementation of strategic change which considers the scope or pace/type and particularly identifies the importance of organizational form with distinct behavioral implications (MacIntosh & MacLean, 1999).

This case study will assess the clarity of long-term goals, resource alignment to long-term goals, the extent of adaptability of the strategy and whether the emphasis in strategic focus is on content (structure) or process, for the three companies that form the substantive focus of the study.

Innovation perspective

In his PhD thesis, Adams (2003) presents an holistic approach to innovation classification. Three innovation types (Readily Adopted, Challenging and Under Cover) form a generalizable framework of innovation, enabling comparison across cases, based on the innovation as the unit of analysis. The benefit of this holistic approach in innovation research is that it enables those items that have traditionally been viewed as discrete (i.e., as multiple attributes) to be meshed in a powerful integrating device. This integrating device is the residue of a thorough analysis of literature research and case study. It ensued from an analysis of descriptions of constructs, construct inter-relationships, organizational contexts, processes from multiple stakeholder perspectives, various data collection methods and levels of analysis. It has enabled the exploitation of the richness of case study (Yin, 2002) and reflected the significance of organizations as complex systems. The analysis provided nomothetic advantages by examining cross-sectional patterns by statistical examination across varying situations (Lucas, 1974) eliminating the lack of generalizability of single cases and enabling generalization to large populations.

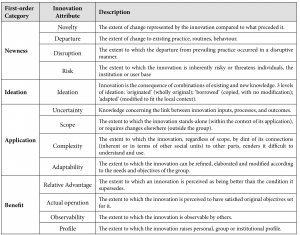

Innovation attributes are classified by four first order categories: Newness, Ideation, Application and Benefit (Figure 1).

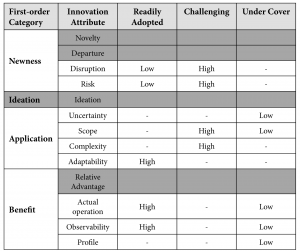

The interesting result that Adams found was that an extensive study of many different innovation cases led to the identification of essentially only three types of innovation. Considering all the a priori possible permutations of the list above (213 if we consider High and Low for each) Adams scores innovations by considering the significance of their underlying innovation attributes. The classification is presented in Figure 2 below. Some innovation attributes are not significant in the classification and are greyed out in Figure 2, others are found to be significantly low or high or not applicable (shown with a dash).

It is the underlying nature of these innovation types that is of primary interest. Adams proposed underlying process characteristics of the innovation types. Readily Adopted innovations have a focus on initiation activities, particularly idea screening and business analysis. Solutions need to mould to local circumstances and the requirement for adaptability is high. The presence of a champion is indicated for Readily Adopted innovations. Challenging innovations are characterized by high ratings for risk, disruption, scope and complexity. They are focused on implementation rather than initiation. Under Cover innovations are notable for an absence of management commitment outside the innovating group although management commitment has been positively associated with innovation success.

There would be considerable interest in examining the reasons why so many potentially possible types are not found. Something like organizational systematics (McKelvey, 1978) or ‘cladistic’ models (e.g., Allen, et al., 2005) may be able to show the incompatibility of certain pairs.

Here, however, we are interested in studying and classifying the innovations identified by the CEOs in their annual reports by evaluating the significance of relevant innovation attributes. The classification allows discussion of the portfolio of innovations which emerges and so the innovation framework is used as a typology facilitating analysis.

Innovation?attributes

Adams, 2003.

{kind=link}

Organizational perspective

The third and final perspective contributing to this case study is the organizational perspective which focuses on the evolution potential of each organization.

Complex systems theory is concerned with the perspective of an organization as a nonlinear dynamical system that is continuously probing its own stability with fluctuations of various kinds. Nonlinearity describes the fact that variables are linked by disproportionate responses. This can either be negative in the sense that a fluctuation is dampened, and the previous condition is stable, or it can be positive, in which case a fluctuation can be amplified and can transform the system structure (Allen, 1994).

In any case, a complex system is always fluctuating. Fluctuation is essential for the existence of a complex system, whether it is at the microscopic, macroscopic or any level between. Our observations of fluctuations in the complex system are time-bound and so we cannot say at any one time that the system is stable or otherwise because of the arbitrary long transients that may occur prior to settling on a particular structural attractor. Fluctuations originate from both within and without the organization. One or more of these fluctuations (or perturbations) in some combination are capable of initiating change and evolution in the organization. Most fluctuations are absorbed and so the emergent structures observed at the macroscopic layer as a consequence of the permitted fluctuations are likely to be robust and significant.

When the current stability of the structure of a system is tested for example when a new idea or practice is ‘trying’ to invade, it encounters a ‘fork in the road’ or bifurcation point. It is at these points that the system can self-organize through unpredictable leaps into different states (Kauffman, 1991). If the old dominant organizational form or attractor basin can dissipate the force or instability then potential changes fail and the system reverts to a variation of its former state. If the new set of influences takes advantage, the forces or energies go into the formation of a new configuration. Bifurcation points and attractors always exist as latent potentials within any complex nonlinear system and they signal the potentials for self-organization and the evolution of new form.

Innovation?types

Adams, 2003.

{kind=link}

A stable organization, that is, one not experiencing much fluctuation relative to its attractor basin is not evolving. It may be surviving and perhaps doing so profitably, however its evolution is uncertain. If the organization’s resources have requisite variety (Ashby, 1962) and are deployed and exploited for the benefits of the organization during times of environmental change, then the organization may continue to exist. This very existence may consume excessive resources and may not be viable or sustainable in the long term.

Any change to the practices or components within a complex system may influence the extant structural attractor of the system. If some bifurcation point occurs and a different structural attractor emerges, this could become the new norm. Arriving at bifurcation will be due to the new combination of components in the system, which themselves may not yet have settled. The system may re-organize to the new structural attractor if it is ‘better’ in some qualitative sense than the extant one. Any re-organization is unpredictable and self-organizing because the relationship between components and the system is nonlinear. And in excessively turbulent environmental conditions, hyper-turbulence can overwhelm adaptive capacity beyond management (McCann & Selsky, 1984).

A particularly strong metaphor for evolution is that of the organization as a biological organism (Morgan, 1997). This metaphor captures the view of organizations as living entities and suggests the existence of different species and of variety. It emphasizes the need for ecology, i.e., understanding the inter-relations between organizations and their environments. The metaphor also suggests that the management of organizations can be improved through systematic attention to the needs that must be satisfied for an organization to survive. This focus on needs encourages the insight of organizations as amalgams of interacting characteristics, including those driven by culture, technology and strategy, which have to be balanced in order to survive. Further, the health of the overall system is dependent on the extent of synergy between such interacting characteristics (Allen, 1994).

The importance of organizational form, that is, the particular set of characteristics that makes one organization similar to or different from another organization, is highly applicable to the process of innovation. When a new invention arises either in the environment or in the organization, the organization’s capability to innovate (or indeed to decide not to innovate) is dependent on its organizational form. And, this is largely dependent on the path along which it has evolved.

The organizational perspective will form the final part of the analysis framework. Key points for identification are:

The fluctuations that exist within each organization and outside it to determine if the organization is evolving or relatively stable;

The attractor basins (or latent potentials) in order to suggest how the organization may evolve;

Whether each organization’s resources have adequate variety to exploit changes in the environment and if the needs are being satisfied systematically;

Whether the interacting characteristics of culture, technology and strategy are balanced, and what synergies are present;

What capacity the organization has to innovate, and;

How its organizational form helps it innovate.

Making these evaluations is limited by the nature of the research. However, the same process is applied without bias to each organization in the case study.

Research method

A grounded, qualitative, inductive approach was taken in examining the public-domain data related to the three organizations in this case study. A breadth in data coverage and data source was the target as the focus on the case study was to identify specific organizational constructs that pertained to evolution. The use of multiple sources permitted some triangulation. However, all data used were public domain, second order data and so my interpretation of this interpreted data will bias my results. My own expectations in using a complex systems lens were to find indications of evolution in:

Modularity and de-composability of components, that will increase the overall fitness of the firm and its capability to mutate Simon (2002);

Integration and aggregation (Holland, 1995) of components in a synergetic manner (Allen, 1994) that is emergent;

Nonlinearity and feedback causing self reinforcing patterns or structures (Arthur, et al., 1987);

Self-organization (Kauffman, 1995) and self-reference in the creation of structure through the process of social construction (Hofstadter, 1979) and;

Components of systemic survival (diversity, inter-dependence, flexibility, cooperation and partnership, and cyclical flow of resources (Capra, 1996).

The primary source of data collection for the company strategy and innovations of each of these companies was the Chief Executive Officer (CEO) statements in current published annual reports. These reports were coded sentence by sentence using content analysis to identify constructs that each CEO (or his writer) had used to describe the evolution of the firm. These constructs were then organized into themes for each CEO report on a within-case basis by clustering constructs that were similar. The specific words and language used in each CEO statement plus frequency and size devoted to the construct, together with the themes, were analyzed in order to arrive at some conclusions as to the relative importance of evolutionary activity of the firm. The emphasis indicated by the CEO of particular evolutionary activity, for example, by stating that this ‘came first’ or ‘was most significant’ was used as a gauge to assess its relative importance to the firm. Each CEO statement was analyzed in this way and triangulated with business reports (via electronic business data sources) regarding these companies. Where anomalies were found between CEO statements and business reports, some scepticism was recorded against the relative importance of the CEO emphasis. In addition, the companies’ web-sites were used to obtain further details of each of the innovations mentioned in the annual reports. Cross-case assessment was carried out as the final stage of analysis to explore the differences and similarities between the cases.

Substantive focus

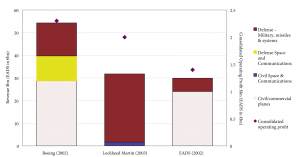

The two primary sectors in the aerospace industry are commercial and defence aviation. Each sector is dominated by two key firms: Boeing and EADS (largely Airbus) in the commercial sector and Boeing and Lockheed Martin in the defence sector (Aerospace Innovation and Growth Team, 2003). Based on figures from their latest annual reports, comparative analysis has been carried out. Note that the figures for EADS are in Euros and that the more recent (2003) Annual Report from Lockheed Martin has been used.

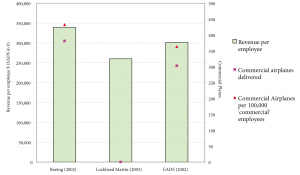

Boeing’s revenues are largely equal between the commercial and defense sectors. Boeing’s revenues in each sector are roughly equal to that of its main competitors: Boeing’s commercial revenue of $28.7bn exceeds that of EADS’s commercial revenue of €24bn and Boeing’s defence revenue of $25.4bn falls short of Lockheed’s defence revenue of $30.1bn. EADS makes 80% if its revenue from the commercial market. Lockheed Martin has 95% of its revenues in the defence market. See Figure 3 for a comparative analysis of revenue. With 166,800 employees, Boeing is by far the largest employer; Lockheed Martin has 130,000 employees and EADS just over 100,000. Figure 4 presents revenue per employee with Boeing achieving the greatest performance. Boeing sold 381 commercial planes and EADS sold 303 in these periods; the number of commercial planes sold per 100,000 commercial employees (determined as the proportion of commercial revenue to total revenue) also shows Boeing as the better performer in Figure 4.

All three organizations aspire to excel, be global leaders or to be the best. With overlapping and competing products, they provide excellent competition for each other.

In commercial aircraft manufacture, manufacturers must produce very high quality, reliable airplanes at competitive prices. Technological innovation and feature differentiation are very desirable but it is more important to remain competitive. Access to global markets and manufacturing process technology is also vitally important. In defence aircraft manufacture, manufacturers must offer aircraft with innovative features that are technologically more advanced. Cost is not of primary concern. Design secrecy is highly important and the prime customer is usually the home country’s Government (Antoine, et al., 2003).

Boeing

Boeing is the largest aerospace manufacturer with turnover twice that of its nearest competitor. Global revenues were $51.1 billion in 2002 of which 53% were generated from Boeing Commercial Airplanes and 47% from Integrated Defense Systems (Boeing, 2003). The commercial/defence portfolio mix has changed markedly since 1993 when 80% was generated from the commercial market. Philip Condit was the Chairman and CEO at the time of the annual report publication but resigned on 1st Dec 2003 at age 62 marking the end of 7 years at the helm. Condit’s resignation followed shortly after his firing of the Chief Financial Officer for alleged unethical practices and the July 2003 punishment by the Pentagon for possessing 35,000 pages of stolen Lockheed Martin documents (Business Week, 2004). A class action accusing Boeing of underpaying female employees and denying them promotions was set to the largest sex-discrimination lawsuit ever to go on trial but has since been settled out of court (Seattle Post Intelligencer, 2004). New CEO Harry Stonecipher is the retired Boeing president aged 67, and was chief of McDonnell Douglas when Boeing bought it in 1997 (Time Canada, 2003). Condit, recognized as a brilliant engineer, moved Boeing from Seattle to Chicago in 2001 (Fortune: Europe, 2003).

Comparative?analysis?of?revenue?and?operating?profit

{kind=link}

Figure?4

Performance per employee

{kind=link}

Philip Condit’s statement in the Annual Report (Boeing, 2003) is entitled “Defining the Future” which has immediate focus on the evolution of the industry. He covers three explicit topics: Strategy, Execution and Markets.

Condit desires Boeing’s strategy to be adequately abstract so as not to have to change frequently. The strategy is to “Excel in All Principal Aerospace Markets.” This has meant creating a diversified company “of unrivalled breadth and balance.” Boeing perceives balance providing greater stability, strength and agility and to this end they have created a company with ‘balanced’ revenue from civil and defence markets. With this diversification comes compromise since each market segment is likely to provide variable levels of profitability and whereas one segment’s profit might smooth another’s loss, overall, profitability cannot be maximal. Condit also retains a technical focus to Boeing’s Strategy requiring the delivery of outstanding performance. Company growth is also identified. The strategy itself has three parts:

Run healthy core businesses, no exceptions and no excuses;

Leverage our strengths to enter new markets where we have the customer knowledge or the technology to make an immediate impact;

Open new frontiers in aerospace with the potential to transform the future.

Boeing put operations first, entering existing markets where they have competencies next and developing new markets last. This is a risk-averse profile, limiting feedback and self-organization.

Condit’s description of Boeing ‘execution’ is centered on customer and investor satisfaction, by “reliability and excellence in financial performance as well as technical performance.” The importance of meeting expectations and taking immediate and decisive action is highlighted, an example being to match capacity to demand following 9/11. The Boeing expectation is of further reductions in commercial airplane deliveries. Lean manufacturing and the introduction of moving lines have reduced final assembly times, an innovation focussed on efficiency improvement and cost reduction, but evidencing integration and aggregation.

Concurrent investment in the future of the business is demonstrated by investment in the new 7E7 and derivatives of existing planes, the Extended Range 747-400ER and 777-300ER.

Condit states that the “best companies … shape the markets of tomorrow.” He recognizes the different characteristics of commercial and non-commercial markets. For commercial aviation and space he notes the prolonged downturn. For defence and non-commercial space, the markets are strong and growing. Condit demonstrates Boeing’s market shaping by the creation of the city-to-city non-stop low-cost and convenience market fragment they have created by airplane range performance improvements, having exploited opportunities in regulatory liberalization.

Condit identifies Boeing Connexion and Boeing Air Traffic Management businesses as having “the potential to transform the future of flight.” Integration in the defence arena is offering “tremendous opportunities … in a networked world of interoperable platforms and systems.” Boeing’s re-organization of military aircraft and missile systems, space and communications businesses into a single organization, Boeing Integrated Defence Systems, demonstrates Boeing’s own belief in integration.

In Condit’s concluding remarks, he looks to the future for Boeing. The anticipation is for solid financial results, demonstrating the balance that the portfolio mix is having for Boeing. Condit answers his own question: “Why am I confident of the future of the Boeing Company?” His answers are: 1. great people, 2. right strategy, 3. good execution, 4. shaping markets of tomorrow, and 5. character and integrity of the company. Although ‘great people’ are cited first, his strategy does not mention the investment in learning and innovation that Boeing provide. These include the Learning Together Programme which is underpinned by Boeing’s Vision 2016 to have the best educated workforce in the world, and the Chairman’s Innovation Initiative which identifies new business concepts and spin-outs and expansion of the intellectual property portfolio by generating new invention disclosures and patent application.

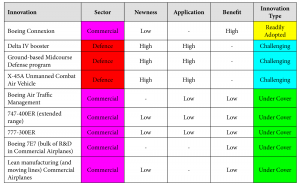

According to Adams’s (2003) innovation framework, Figure 5 below is presented as an analysis of the innovations identified in the Boeing annual report (2003). The innovation types were determined following an assessment of the apparent significance of the innovation attributes (disruption, uncertainty, etc.—see Figure 2) as discussed in Boeing’s annual report. Each innovation could be classified by Innovation Type. A discussion appears after the EADS and Lockheed Martin summaries.

{kind=link}

EADS

EADS is the second largest aerospace and defence company with turnover of €29.9 billion (European Aeronautic Defence and Space Company EADS N.V., 2002). With 1 Euro worth around 1.04 USD, the exchange rate was close to par at the end of 2002. The Euro is now stronger and exchanges for approximately 1.28 USD (2006). Around 80% of EADS revenues arise from the commercial market to which Airbus contributes significantly. EADS are moving towards an expected financial recovery.

EADS, with head-offices in France and Germany, has two Chief Executive Officers—Philippe Camus and Rainer Hertrich. A recent article, one of a very few relating to EADS, finds Camus endorsing the creation of a European armament, military capabilities and research agency to combat tighter US technology transfer restrictions (Aviation Week & Space Technology, 2003).

The “Message from the CEOs” in the Annual Report is organized into a question and answer format. It covers the EADS activity in three markets—Defence, Civil and Space—and then explores the strengths and strategy of EADS.

Although the building up of the defence side of EADS is a strategic priority, the CEOs recognise the nature of defence projects as long-term and subject to political change. Completed projects include the creation of MBDA, the 2nd largest missile systems company in the world. The importance of partnership is recognized and include partnerships with BAE Systems and Finmeccanica. Preferred bidder status with the UK MoD (Ministry of Defence) is expected to help their breakthrough into all European Markets and even NATO. The creation of North American EADS is expected to improve market access to the US and particularly to gain access to US technology. These comments from the CEOs recognise the need for systemic survival, in particular co-operation and partnerships.

The CEOs note that the A400M programme in Germany is expected to “trigger synergies with Airbus civil activities.” The Airbus fleet has a unique advantage of operational commonality, leading to savings for operators in terms of crew training and improved efficiency and flexibility. This recognizes the need for modularity in complex systems.

The Civil market is described as lackluster, driving production down 22% to 303 aircraft albeit up on market share. The down-cycle is harsh and unpredictable, but Airbus state that they are in better shape than ever to manage it, particularly by productivity improvements and benefits of scale. Development of the very large future aircraft A380 is self-financed, entering peak R&D and capital expenditures. Increased demand for Eurocopter places it holding 60% of market share in this segment.

Space business is the most challenging for EADS, suffering from both over-capacity and lower demand. EADS’s launcher business is directly affected by the difficult satellite telecommunications market and by the problems with the new Ariane 5 ESCA launcher that are being worked on. Opportunities are expected to deliver in programmes like Paradigm and Galileo.

The strategy for global leadership has been pursued successfully, despite the difficult environment, due largely to EADS’s capacity to react and adjust to uncertainties and the building of a strong, united company. A clear vision over growth is expected via EADS International, which supports marketing around the world, and works across divisional boundaries. EADS is ambitious to achieve and maintain global leadership, but also to take a realistic approach recognizing the unpredictable nature of the world. The CEOs recognise that feedback occurs and there is need for flexibility. Tactics are to look for cost savings and cash generation where growth is not available and to give demanding development targets where growth prospects exist. EADS recognizes its main strengths as successful products and quality of their people.

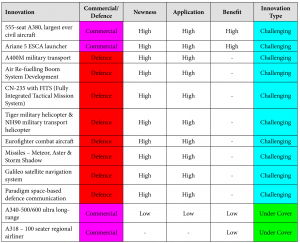

Figure 6 below is presented as an analysis of EADS’s innovations using the same innovation framework and method as for the Boeing assessment.

The discussion appears after the Lockheed Martin summary.{kind=link}

Lockheed Martin

Lockheed Martin Corporation is the third largest aerospace manufacturer with turnover of $31.8 billion in 2003 (Lockheed Martin Corporation, 2003). 95% of their business is in the defence market. Lockheed Martin CEO Vance D. Coffman was named Chairman on 24th April, 1998, succeeding Norman R. Augustine who remained a director (The Wall Street Journal: Eastern Edition, 1998). Coffman retired on 6th August, 2004, and Robert Stevens has taken over as CEO.

At the top of Lockheed’s priorities is customer satisfaction as stated by Coffman in the Annual Report. This is aided by the creation of Integrated Systems & Solutions and the Global Vision Network that are enabling collaboration among customers and Lockheed. Lockheed are keen to manage expectations and note that, as a government contractor, they are subject to oversight but that Government indemnification does not cover all risks.

The commercial launch vehicle market place is recognized as very competitive with low demand for new satellites and excess capacity in the telecommunications industry. Opportunities are identified in space exploration. Defence business, in particular military missions and reconstruction in Iraq and Afghanistan, is strong. The emphasis on homeland security is expected to increase demand for Lockheed’s capabilities in air traffic management, ports and waterways security, biohazard detection systems for postal equipment and information systems’ security.

Lockheed has sold its commercial IT business to ACS in a transaction where Lockheed bought the defence and most of the civil government IT business from ACS. There is apparent focus on network-centric solutions for defence and national security customers and on Citizen-centred civil government solutions using capabilities in critical intelligence, knowledge management and e-Government. Both these solution types recognise the need for integration of complex systems. There is expected growth in business-process outsourcing due to legislative change in public/private competitions and from the government in upgrading and investing in new information technology systems and solutions. Lockheed are continuing to focus resources in support of infrastructure modernisation, allowing interoperability and communication across agencies. Finally, opportunities are also identified through organizational changes, where Lockheed can leverage technical expertise across the organization.

Lockheed?Martin?innovations

{kind=link}

Market focus is demonstrated by the reorganization of Lockheed’s business areas to address the “changing and increasingly complex needs of our defense customers, especially in the critical area of Information Superiority.” Lockheed’s focus as a lead systems integrator recognizes the emerging priority of the US Department of Defense towards “joint operations, net-centric command and control and integrated capabilities of the armed forces.”

Innovation is evident in the multiplicity of solutions. Globalization and internationalization is demonstrated by the creation of the “Global Vision Network ... and the Global Vision Integration Center in Suffolk, Virginia.” The skills of “this innovative corporation of 130,000 dedicated men and women… who bring a passion for invention” and recognition that a “diverse and talented workforce is fundamentally important to our future competitiveness”; and “superior development processes (and process improvement).”

Customer satisfaction and operational performance are high on the list of priorities. These are achieved by recruitment and retention of the best people, the use of efficient methods, such as lean manufacturing techniques, the importance of values to inspire the management team and ethics and the importance of social responsibility.

Coffman’s vision for Lockheed to be the “best advanced technology systems integrator” is consistent with the focus in resources. Coffman reflects on the successful execution of their strategy of disciplined growth evidenced with a third straight year of positive momentum in sales and operating profit. Coffman is now handing over and is “confident that the future of Lockheed Martin is indeed bright and the best years are ahead.”

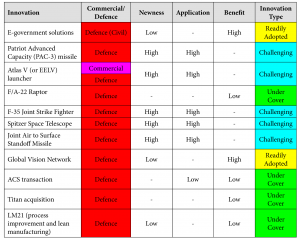

Figure 7 above is presented as an analysis of Lockheed’s innovations using the same innovation framework and method as for the Boeing assessment. The discussion appears below.

Just one year prior to his handover of the chairmanship to Coffman, Augustine handed over the CEO reigns to Coffman. At this time he offered 12 suggestions for the survival of the US defence industry (Augustine, 1997). These suggestions are identifiable and aligned with Coffman’s final CEO statement. Coffman’s recognition of the importance of social responsibility is the only item Augustine does not mention.

Discussion

Boeing’s move from 80/20 commercial/defence revenues in 1993 (roughly the same as EADS has in 2002) to 53/47 in 2002 is consistent with the strategy of reducing dependence on the cyclical commercial airplane market. However, it is fortuitous that Boeing had reduced its exposure to the commercial market by the time of the 2001 terrorist attack in New York that prompted a significant downturn in civilian travel but an upturn in the defence market. Boeing’s resources had adequate variety to exploit the changes in the environment and were aligned with the change. Further demands for integrated solutions in the defence market have prompted a re-organization within Boeing and the creation of a new business unit that should help it to innovate further. This is particularly important in the defence market. In terms of strategic thinking, Boeing’s strategy is driven by content/structure and traditional economic rationality.

An analysis of Boeing’s 9 innovations reveals Boeing’s focus in the commercial market. 67% of its innovations are in the commercial sector although its revenues from this sector amount to only 53%. This can indicate its desire to strengthen its commercial market position. All 3 defence innovations are Challenging innovations, indicating a focus on implementation. There is an absence of Readily Adopted innovations in the defence industry innovations which signals a search for generic defence solutions rather than locally customizable innovations. All bar one of the remaining 6 innovations are Under Cover innovations. Adams (2003) found an absence of management commitment (outside the innovating group) in Under Cover innovations and if the same is true for these innovations, there are implications for Boeing given the number of such innovations, assuming that the assessment of innovation type is correct. Only one innovation is Readily Adopted and this is in the Commercial sector. This indicates that there is a product champion for Boeing Connexion and that it is highly adaptable innovation.

There is evidence that interacting practices of culture, technology and strategy are balanced however Condit does not mention that Boeing are building a Global Enterprise (Boeing, 2003). Also, its investments in technology-focussed venture capital funds are not reviewed by the CEO and these are potentially key sources of innovative strength. How these fit with ‘Execution’ is also not clear. The strategy does not consider how market demand for commercial and military aircraft may change in the medium and long-term. If the safety and security features being developed now are implemented in the short-term and more people are encouraged to fly, then the mix should will favor commercial aircraft in the medium-term. In the long-term however, commercial flight may be significantly curtailed because of escalating environmental conditions aggravated by airplane emissions. Homeland defence demand is unlikely to be curtailed in this way. Boeing’s strategy for a balanced portfolio will keep options open to them.

Perturbations within Boeing include the dismissal of the Chief Finance Officer and the resignation of the CEO. This is particularly poignant as the CEO described the importance of integrity in his annual statement. These departures are likely to push Boeing into a new evolutionary direction. The resurrection of retired Boeing president Stonecipher as the new CEO will be a holding position that is intended to bring some stability in the light of outstanding actions and thus will pull Boeing back to its existing attractor basin. This move will stifle evolution and enforce risk aversion. Until a new CEO is appointed Boeing is unlikely to evolve.

EADS is vulnerable to the lower demands for civil airplanes and satellites/launchers because of its exposure to this market segment. These fluctuations outside the organization are reflected in the cutting back of production and greater need for productivity efficiencies within EADS. There is some mitigation due to successful growth in the defence market and in the Eurocopter. Overall, EADS is unlikely to be in a stable situation and it is likely that structural attractors favoring the defence market and customized personal transport (such as the Eurocopter) will be stronger.

An analysis of EADS’s innovations highlights the company’s focus on defence market implementation. For an organization that achieves 80% of its revenue from the commercial sector, only 33% of its innovations are in the commercial sector. This indicates the company’s push into the Defence market. Of the 12 innovations, 10 are Challenging innovations, and all innovations in the defence market are Challenging innovations. Of the 4 commercial innovations, 2 are Under Cover innovations; these are the long-range and the regional airplane projects. The absence of Readily Adopted innovations could indicate the lack of product champions in EADS. The innovation portfolio is unbalanced across innovation types and across markets signalling the potential for significant internal fluctuation.

EADS is exposed to the civil airplane market, however it has weathered storms before and can perhaps withstand fluctuations in demand. Culture and technology appear to be balanced and a strategy to grow defence using innovative staff is synergetic. This demonstrates a more process-driven strategy. The organization invests substantially in research and development and obtains grants for research. If progress in the space market does not materialise, there will be a structural attractor away from this work and maintaining a position in this market will be difficult.

In the medium-term, the structural attractor of the civil airplane market is likely to strengthen for EADS as security improves and demand increases, particularly for long-haul cheap flights. The A380 may arrive with perfect timing, but will require the adaptive ability of the organization to exploit it fully. In the long-term, the growth of the defence (and space) business is the only area for evolution, and this is already reflected by the focus on defence market innovations.

Lockheed Martin has experienced significant recent growth of nearly 20% in 2003 and 11% in 2002. This is a reflection of the demand in defence and military aircraft and the capability of Lockheed Martin to deliver to demand. This strengthens the structural attractor that demands innovative staff. The organization has also recognized two major new drivers for change—the demand for integration systems and the civil government agenda for electronic service delivery. These have been recognized by acquisitions (and disposals) which strengthen the capacity of the organization to evolve in this direction.

An analysis of Lockheed’s innovations presents a balanced innovation type portfolio. All 11 innovations are focused on the Defence market, although the Atlas V launcher can be used in the commercial market. There are two Readily Adopted innovations, which focus on initiation and have high adaptability. There are 5 Challenging innovations that are highly product focussed and demand implementation attention. There are 4 Under Cover innovations, which demonstrate an absence of management commitment outside the innovating group and interestingly these are focussed more on process innovation.

Lockheed recognizes the increasing complexity of the needs of their defence customers, particularly with respect to information superiority. Lockheed is addressing this by organizational changes to their workforce. There is evidence of content-driven strategy, for example, the creation of Integrated Systems & Solutions and the Global Vision Network, but there is also some evidence of process-driven strategy and the encouragement of behaviors that will enable organizational forms to develop. Culture, technology and strategy are closely balanced and provide synergies. The recent departure of the CEO will bring an internal fluctuation which could cause the organization to evolve in a new direction or more rapidly into integrated systems. Long-term the current growth rates are unlikely to be achieved as defence and military needs reduce. The development of integrated systems may provide the structural attractor for evolution.

{kind=link}

Conclusions and limitations

Figure 8 below summaries the strategy, innovation and organizational perspectives reviewed in this case study. The assessments are relative to the companies examined (not absolute values), and were interpreted from the text of the company annual reports. There is no ‘right’ assessment for any of these criteria since they are contextual.

Boeing maintains that a balanced portfolio across defence and civil markets has given it stability, strength and agility by the creation of a diversified company. But with diversification comes integration cost which EADS has dealt with somewhat in its approach to operational commonality. EADS is looking to increase its share of the defence market so that it achieves 30% (from 20%) of revenue from defence and is innovating aggressively to achieve this. Lockheed is almost entirely in the defence market, although there is clearly much activity in integrated systems , both within the military and civil government. Boeing too have reorganized around the integration scenario although their’s appears to be a structural integration rather than a technological integration. As at 2002/3 most profits were made from the defence market and so EADS suffered most, and recognizes its need to improve its exposure to the defence market.

Each supplier is exploring one or more market niches: Boeing Connexion and Boeing Air Traffic Management projects; EADS’s Missile systems and Eurocopter, plus the A380; Lockheed Martin’s Global Vision Network and e-Government solutions.

Operational demands for performance and efficiency are evident for all suppliers. EADS had adapted is production levels and is improving efficiency in its civil business. Boeing is focussed on financial and technical performance and on taking immediate action on market changes. Lockheed Martin states the need for operational performance and efficient methods but these diminish under the focus of innovation and growth opportunities. Boeing and EADS are both relatively agile as has been demonstrated by action to respond to reduced market demand. EADS’s desire for agility is reflected in the frustration it feels at the anticipated long-term quest to penetrate the US defence market. Lockheed Martin shows less agility and more risk awareness and aversion although these are balanced somewhat by a passion for innovation. Boeing is also passionate about innovating and opening new frontiers, but its first priority is to run healthy core businesses.

In terms of differences, EADS is the only organization that mentions partnerships and is using these particularly to gain access to wider markets. EADS is the only one to recognise synergies explicitly from defence across to Airbus. Lockheed Martin is the only one engaged in acquisitions and disposals. Lockheed Martin is alone in its explicit corporate social responsibility statement.

EADS appears to be placing most energy into evolution, and is most process focused in its strategic outlook. As such, it may evolve most significantly. In particular, developments as a consequence of its 555-seater plane, and its push for defence market share provide significant latent potentials. Boeing is likely to stagnate in the short to medium-term as it redefines its corporate identity under new leadership. Its commercial market operational focus and innovation portfolio is inhibiting significant innovation. Lockheed Martin is currently evolving successfully because of defence market demand, but this is likely to peak and may contract in the long-term. Civil government and integrated solutions could provide Lockheed’s new evolutionary pathway.

This case study has explored the evolutionary potentials of the three largest aerospace manufacturers by evaluating strategic focus, innovation portfolio and organization potential for evolution. Both within-case and cross-case evaluations have been carried out based on public information within mostly Company Annual Reports. My contribution has extended Adams’s (2003) work into a new organizational context.

Further research could explore these organizations’ innovations more deeply and perhaps create a matrix of innovations for each organization enabling a more accurate analysis of innovation portfolios. The analysis of the innovations in the three annual reports is limited by the innovations specifically identified by the CEOs and by their descriptions of these innovations. Those working in the companies would be able to provide comprehensive details of all innovations and would be better able to classify them (according to Adams) resulting in a more accurate analysis. In particular a large limitation of the research is that the amount of investment or emphasis placed on each innovation is taken as equal, where in practice this is unlikely to be the case. The authors do not have access to the detailed spend on each innovation nor its importance with regard to the evolution and sustainability of the firms, therefore the conclusions are somewhat speculative. The relationships between the innovations and organizational forms of each of these companies could be studied to identify more clearly the developing latent potentials. Unexplored environmental factors could also be considered.

Although the source text is indisputable, the authors’ interpretation of the text may differ from either the intended interpretation or a consensus of constructions of the text. To moderate this, the organizations themselves could rate the assessments of their organizations, strategies and innovations and indicate whether they perceive the same constructs and evaluations as the authors. Other raters, both with a complexity lens and with other lenses, for example, resource-based view or contingency perspective, could rate the annual reports and consider evolutionary potential. These analyses would provide a richer more meaningful interpretation. In any event, the source text is confirmable (capable of being tested and verified by access to the public documents) and the process used for analysis in the study is consistent and repeatable (Miles & Huberman, 1994). As our understanding of complex systems evolves, we are likely to produce different results over time.

The value of the organizational analysis is limited to the complex adaptive systems perspective. The evolutionary approach taken and, in particular, identification of what might lead to bifurcation points for these companies, is subjective.

There is limited generalizability from the sample of aerospace manufacturers to all aerospace manufacturers since it is the largest 3 firms that are examined and so are not representative of the population as whole. There are strictly limited inferences that can be made about motivation or intent as a consequence of the content analysis. A larger, quantitative study of the industry could ameliorate sample limitations.

Application of the innovation framework (Adams, 2003) is potentially limited for the aerospace industry since innovation types were concluded from research into NHS innovations. The NHS is the largest employer in the UK and organized into many departments and services. This does not compare in size, location or industry sector to aerospace and so it is likely that the innovation framework would have at least some differences in morphology if it had been conducted in aerospace firms. However, if confirmed, the innovation framework provides a valuable, integrated insight into a key aspect of organization evolution, that of innovation.